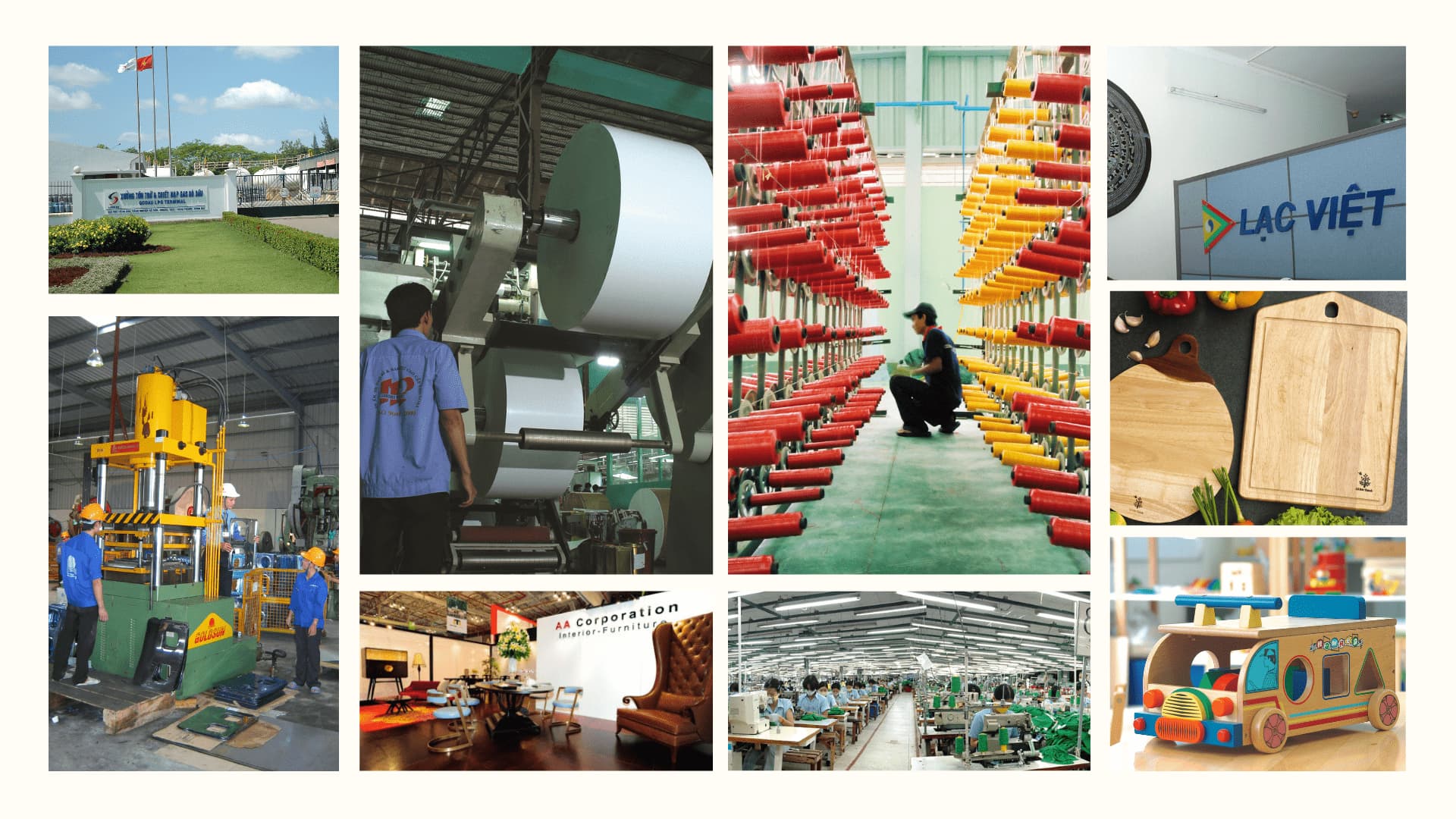

First fund in Vietnam to focus uniquely on investing in private companies

Seeing the opportunity to set up the first fund in Vietnam to focus uniquely on investing in private companies, Mekong Capital launched the Mekong Enterprise Fund (MEF) in 2002 at US$18.5 million in committed capital.

MEF was fully invested in 10 companies by the end of 2005. These tended to be export-oriented manufacturing companies that were family-owned.